This week King World News interviews James Dines, Michael Pento, Rick Rule and Chris Whalen. These interviews discusses the Japan devastation, rebuilding, real inflation in the U.S., depreciation of the dollar (breaking below support), Uranium, Loan modifications and bank balance sheets. Great interviews that hit multiple facets of the economy, really highlighting the issues in todays economy.

James Dines - Discusses Japan situation due to the disaster that has happened. Also, BOJ starting printing additional money to clean up this effort, which is helping cause further inflation. James talks about the worries that are occurring in our nations food supply and the increasing prices effecting availability. He also talks about how turning food into energy is creating further shortages in food and increases in price. James sees silver going well over $100 per ounce. James also discusses this race to rearm weapons all over the world like in the 1930's. James points out that people that don't understand currencies will participate in the biggest wealth transfer in history (on the losing end). James points out that Gold is money and regardless of price, it will always be the central part of money.

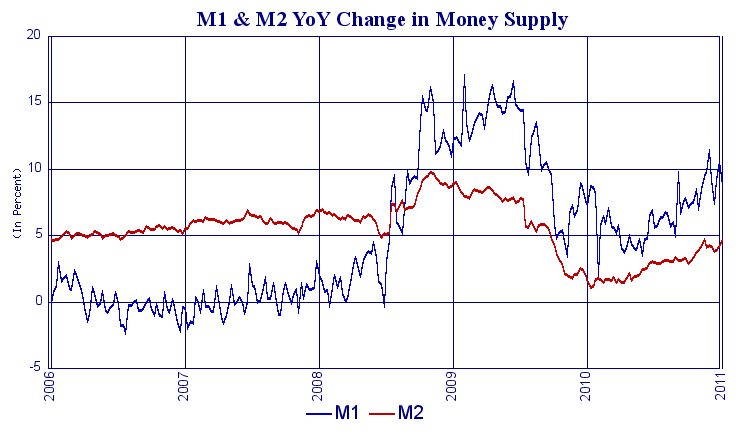

Michael Pento - Discusses how Japan is the 2nd largest country holder of our debt (approx $900 billion). He says they should be a seller of the bonds to use the money to rebuild and further their economy, but instead they have printed 31 trillion Yen in the last 3 days depreciating the value of the Yen. Michael asks who is going to be a purchaser of debt if the Treasury needs to continue to sell bonds (as Japan will be busy rebuilding). Michael says that the U.S. will be paying 50% of our revenue, just to service the interest on our debt. Michael believes for some form of default on its outstanding national debt in the future. We also hit a 52 week low on the Dollar index (below 76) which is a bad sign (broke through support). Michael points out that most Americans have no real retirement and will rely on Social Security which will not be there for them. Government inflation numbers do not really reflect true inflation and the FED is over its stated 2% even with the corrupt calculation of CPI and PPI today. Michael says we are actually at 9% inflation currently.

Rick Rule - Discusses Japans nuclear accident and its effect on Uranium prices around the world. Pre-Japan, Rick was bullish on energy and post-Japan Uranium has increased over 50% which he believes is due to an on-going bull market in Uranium. 20% of our energy in the U.S. comes from Uranium/Nuclear power and if we were to turn off these plants tomorrow, we would not have electricity. Rick goes on to make the case for long term investment in Uranium, but short term it may go down as emotional concerns weigh in.

Chris Whalen - Discusses the organized (or not) investigation in mortgage origination and servicing. Chris believes this is mostly political fluff and the Attorneys General don't have enough of a case here. Chris points out with all this loan modification, how are we not marking to market the whole portfolio creating accounting issues. Chris mentions we will continue seeing foreclosures for some time, which will impact bank earnings (expenses in foreclosures hitting earnings). Chris also talks about why did we let these banks get so big in the first place (too big to fail) creating and reinforcing their monopoly in the finance industry. Chris brings up that currently when a loan is originated the loan is sold off to another institution (Fannie Mae/Freddie Mac) along with the servicing (usually a big bank), but servicing should be retained by the local bank that it originated. Chris points out that if the limit for conforming jumbo loans is decreased in September, we will see housing prices decrease until the end of the year ( instead it the cap should be increased to 1 million dollars). Very critical information from Chris on the banking industry and aiding your understanding of it.